The 2026 tax submitting season is formally open, and for hundreds of thousands of People, the envelopes arriving in mailboxes (or the notifications pinging telephones) are going to include a nice shock.

Due to the laws handed final July—formally generally known as the One Large Lovely Invoice Act—refunds are projected to be considerably bigger this 12 months.

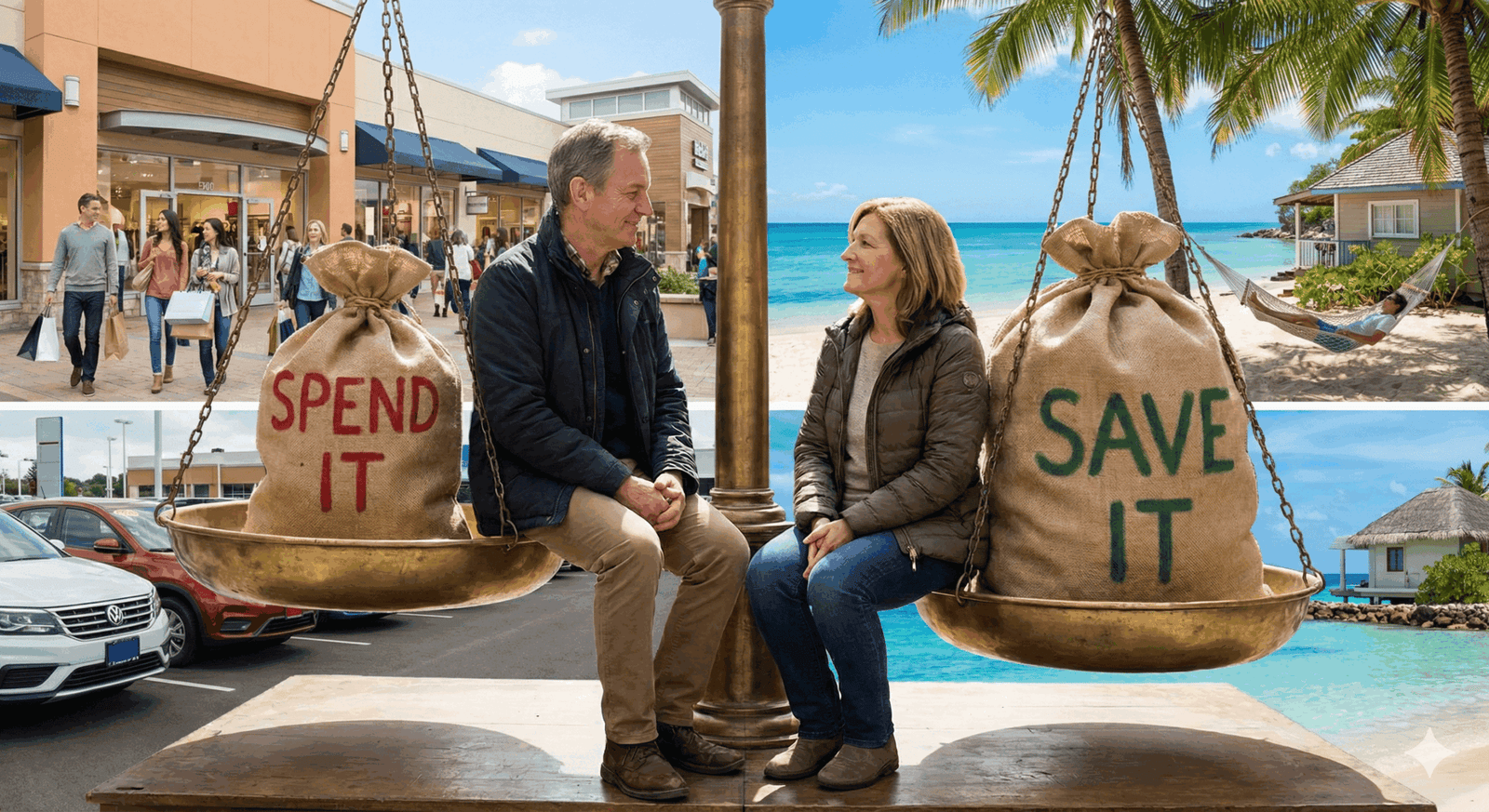

Whereas getting a fats test from the Treasury appears like profitable a mini lottery, I’m going to be the buzzkill good friend who reminds you of the reality: A tax refund just isn’t a present. It’s an interest-free mortgage you gave to the federal government for the final 12 months.

However for the reason that cash is coming again to you, the neatest play is to place it to work. Right here is why your test is probably going greater this 12 months — and 5 particular methods to make use of it to construct precise wealth.

Why your refund is greater this 12 months

The Large Lovely Invoice launched sweeping modifications to the tax code mid-year, which suggests your paycheck withholding possible didn’t modify quick sufficient to maintain up. Once you file your 2025 return this spring, you might be catching up on these breaks.

First, the usual deduction saw a massive jump to $15,750 for singles and $31,500 for married {couples}.

Second, new deductions for working-class earnings took impact retroactive to Jan. 1, 2025. For those who work within the service business or pull lengthy hours, the brand new “No Tax on Ideas” and “No Tax on Extra time” provisions imply earnings you already paid taxes on through withholding is now successfully tax-free (as much as sure limits), triggering a refund.

Add within the new deduction for automobile mortgage curiosity and the expanded Child Tax Credit of $2,200, and the mathematics tilts closely in your favor. The Tax Basis estimates these modifications decreased particular person taxes by roughly $129 billion for 2025, a lot of which is coming again as refunds proper now.

So, you’ve gotten the money. Now, what do you do with it?

1. Destroy your high-interest debt

That is the unsexy, non-negotiable first step. In case you are carrying a steadiness on a bank card, you might be possible paying upwards of 20% curiosity. There is no such thing as a funding on this planet that ensures a 20% return, however paying off that debt does precisely that.

Utilizing your refund to wipe out a $3,000 bank card steadiness isn’t simply “spending” the cash; it’s shopping for your self freedom from month-to-month funds. For those who ignore this and purchase a brand new TV as a substitute, you might be basically financing that TV at 20% curiosity. Don’t do it.

2. Absolutely fund your emergency brake

We frequently name this an emergency fund, however consider it as an emergency brake. When life spins uncontrolled—a layoff, a blown transmission, a medical deductible—this money stops you from crashing into debt.

Surveys constantly present {that a} terrifying share of People can’t cowl a $1,000 emergency with money financial savings. In case your refund is substantial, deposit it immediately right into a high-yield savings account that’s separate out of your checking.

Goal for 3 to 6 months of dwelling bills. If that feels unimaginable, begin with $1,000. It’s the buffer that retains a foul week from changing into a foul 12 months.

3. Feed your Roth IRA

In case your debt is gone and your financial savings are safe, take a look at your future. A Roth IRA is likely one of the finest automobiles for this since you contribute with after-tax {dollars}—which is precisely what your refund is.

You’ll be able to contribute as much as $7,000 (or $8,000 if you’re 50 or older) for the 2025 tax 12 months up till the April submitting deadline. The great thing about the Roth is that your cash grows tax-free, and you may withdraw it tax-free in retirement. Utilizing a refund to max this out is like taking cash the federal government gave again to you and placing it the place they’ll by no means contact it once more.

4. Put money into residence worth, not simply decor

For those who personal a house, it’s tempting to make use of a windfall for brand spanking new furnishings or a beauty refresh. As an alternative, search for unglamorous improvements that actually add value or prevent cash.

Contemplate energy-efficiency upgrades. Issues like sealing drafts, including attic insulation, or upgrading a thermostat pay you again each month in decrease utility payments. For those who use your refund to repair a leaky pipe or change a dying water heater earlier than it floods your basement, you might be performing a “preventative funding” that saves 1000’s down the street.

Repair your W-4

When you’ve determined what to do along with your massive refund, don’t neglect to make sure you don’t get one subsequent 12 months.

I do know, it feels good to get that test. However when you get a $3,000 refund, meaning you lived on $250 much less per thirty days than you truly earned all 12 months. That’s $250 you could possibly have used to pay down debt month-by-month, make investments, or just deal with rising grocery prices.

Go to your HR division or use the IRS tax withholding estimator to regulate your W-4 kind. The aim is to interrupt even—to pay precisely what you owe and never a penny extra. Hold your cash in your pocket the place it belongs, not in Uncle Sam’s interest-free vault.

There’s just one exception: For those who simply can’t appear to handle your cash from month to month and rely on that annual money infusion, tremendous. Go forward.

However it could be good when you didn’t give Uncle Sam an interest-free mortgage yearly. In spite of everything, he’s not doing that for you.

Trending Merchandise